Investing on Limited Cash Flow: A Guide for Early-Career Professionals

This article originally appeared in expanded form on Shaun's financial education site, Melby Money.

Many of the early-career professionals I work with at Melby Wealth Management have a strong long-term earning trajectory and very little monthly cash flow available to invest right now. Medical residents, junior associates, and first-year tech employees all share a similar pattern: high future income potential, meaningful current debt, and limited investable savings during the years when compounding does its heaviest lifting. As a CERTIFIED FINANCIAL PLANNER™ (CFP®) professional running a fee-only fiduciary firm in Nashville, my goal in writing this is to lay out a framework for that exact situation.

Why Starting Small Still Matters

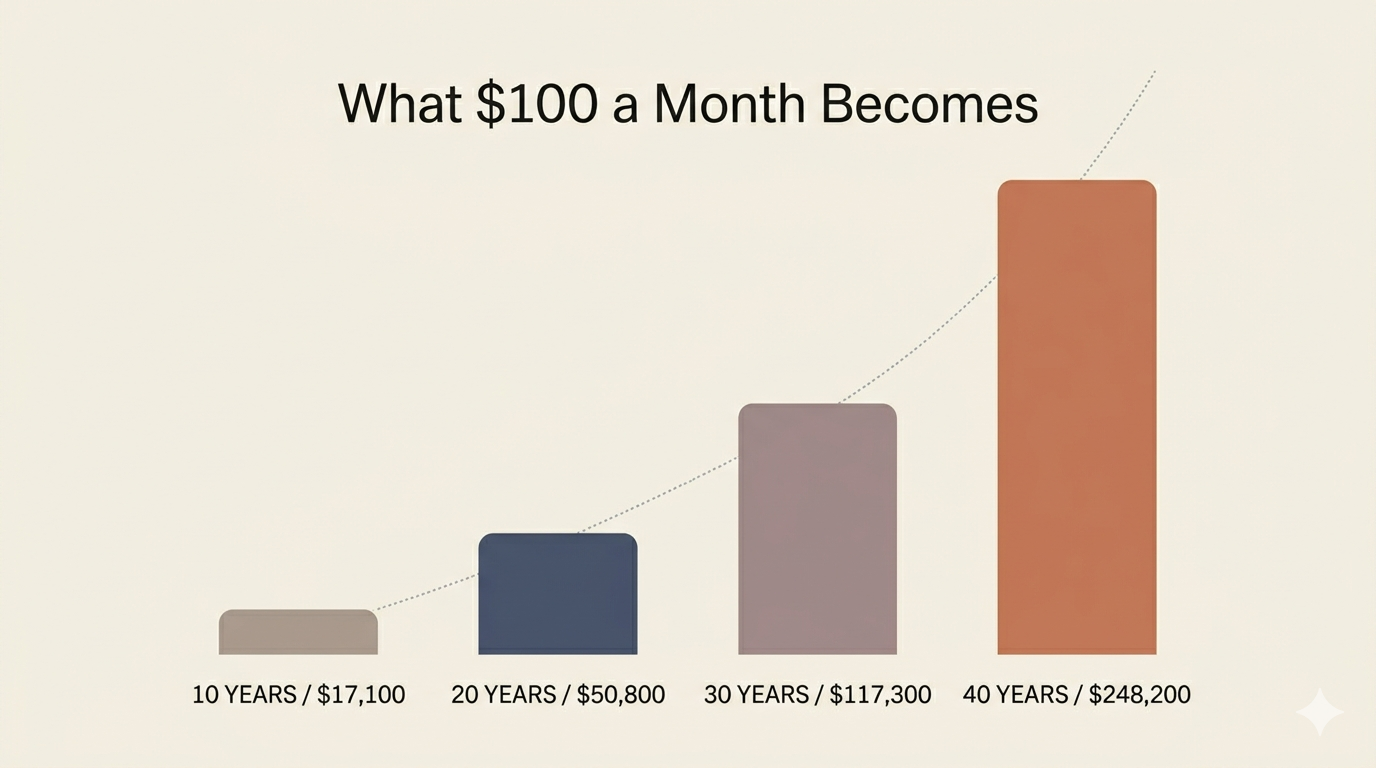

Even at $100 a month, the math is meaningful. Using the Fisher equation to convert the S&P 500's roughly 10% nominal historical return to a 6.8% real return, $100 monthly compounded over 40 years grows to approximately $248,000 in today's dollars. Doubling the contribution to $200/month grows to roughly $497,000 over the same period.

Hypothetical projections only. Past performance does not guarantee future results. Actual returns will vary.

Hypothetical only. Past performance does not guarantee future results.

Time matters more than dollars in the accumulation phase. A resident who contributes $100/month for the four years of training and steps it up to $1,000/month afterward will substantially outperform a peer who waits until residency ends to start. The first contributions get the longest runway.

The Account Order I'd Generally Recommend

For an early-career professional with limited monthly cash flow:

Capture any 401(k) or 403(b) match available, even if the match is small. This is the single highest-return move in personal finance.

Fund a Roth IRA if your income qualifies. The 2026 contribution limit is $7,500. Single-filer phase-out runs from $153,000 to $168,000 of modified AGI; for married filing jointly, $242,000 to $252,000. For someone in the 22% or 24% federal bracket who expects to be in the 32% or 37% bracket later in their career, paying tax now to lock in tax-free growth is generally a good trade.

Build a starter emergency fund in parallel. One month of expenses is a reasonable initial target while you continue to invest.

Address high-interest debt. Credit card balances and any debt at 8% or above generally deserves to be paid down before adding to a taxable brokerage account.

This is a starting framework. The right sequence shifts based on the specific debt structure (federal vs. private student loans, refinance availability, forgiveness program eligibility) and the specific income trajectory.

What to Hold

For a young professional with limited investable cash, a single diversified, low-expense-ratio total U.S. stock market ETF is generally a reasonable holding. The Vanguard Total Stock Market ETF (VTI), for example, has an expense ratio of 0.03% and provides exposure to roughly 3,500 U.S. companies in a single trade. Schwab and Fidelity offer comparable products. The complexity of asset allocation grows over time. For now, the priority is getting the contributions running automatically and consistently.

When Professional Guidance Adds Value

For someone with $100/month to invest, a fee-only financial advisor probably adds limited near-term value relative to a single ETF in a Roth IRA. The case for engaging earlier rather than later is different. It is about setting up the architecture before income peaks:

Tax strategy. Backdoor Roth eligibility, asset location across taxable and retirement accounts, and the tax impact of equity compensation when it begins.

Coordinated planning. Connecting investment decisions with insurance, estate planning basics, and student loan strategy. For physicians, attorneys, and tech employees, the right student loan refinance or forgiveness decision can outweigh the investment return for several years.

Behavioral coaching. The investors who underperform their funds the most do so during the first market downturn after they've built a meaningful balance. Having a fiduciary in your corner before that moment matters.

The cost of a fee-only firm at this stage is real. The value is mostly forward-looking. Most early-career professionals who eventually engage with us wish they had done so two to three years earlier.

What to Do Next

If you're at the beginning of a high-earning career and the constraint right now is cash flow rather than knowledge, the framework above is a reasonable starting point. As your situation gets more complex, professional guidance starts paying for itself.

If you'd like to talk through your specific picture, we're happy to have that conversation.

For the consumer-facing version of this post, head over to Melby Money.

About The Author

Shaun Melby, CFP® provides fee-only financial planning and investment management services in Nashville, TN through his company Melby Wealth Management. Shaun has over 15 years of experience as a financial advisor in Nashville. Shaun created Melby Money to educate the public about finances.

Full Disclosure: Nothing on this website should ever be considered to be advice, research, or an invitation to buy or sell any securities. Please see the Disclaimer page for a full disclaimer.