Retirement Planning: Building Your Long-Term Financial Strategy

What most of the households I work with want, when they first sit down with me, is a plan. Not more information. Not another spreadsheet. A plan they can act on, with someone in the room who can answer the questions as they come up.

For most new client engagements at Melby Wealth Management, retirement planning is where that conversation starts. Not because retirement is the most interesting part of the plan, but because it is the load-bearing wall the rest of the plan attaches to. Equity comp, business sale proceeds, education funding, charitable giving, estate planning, every one of those decisions changes when the retirement endpoint comes into focus.

As a CERTIFIED FINANCIAL PLANNER® (CFP®) professional running a fee-only fiduciary firm in Nashville, my goal in writing this is to articulate what retirement planning actually looks like at the household level when there is real complexity in the picture: multiple account types, equity compensation, a business interest, a working spouse, and meaningful taxable assets alongside the qualified accounts.

The Number Is the Easiest Part. The Sequencing Is the Hard Part.

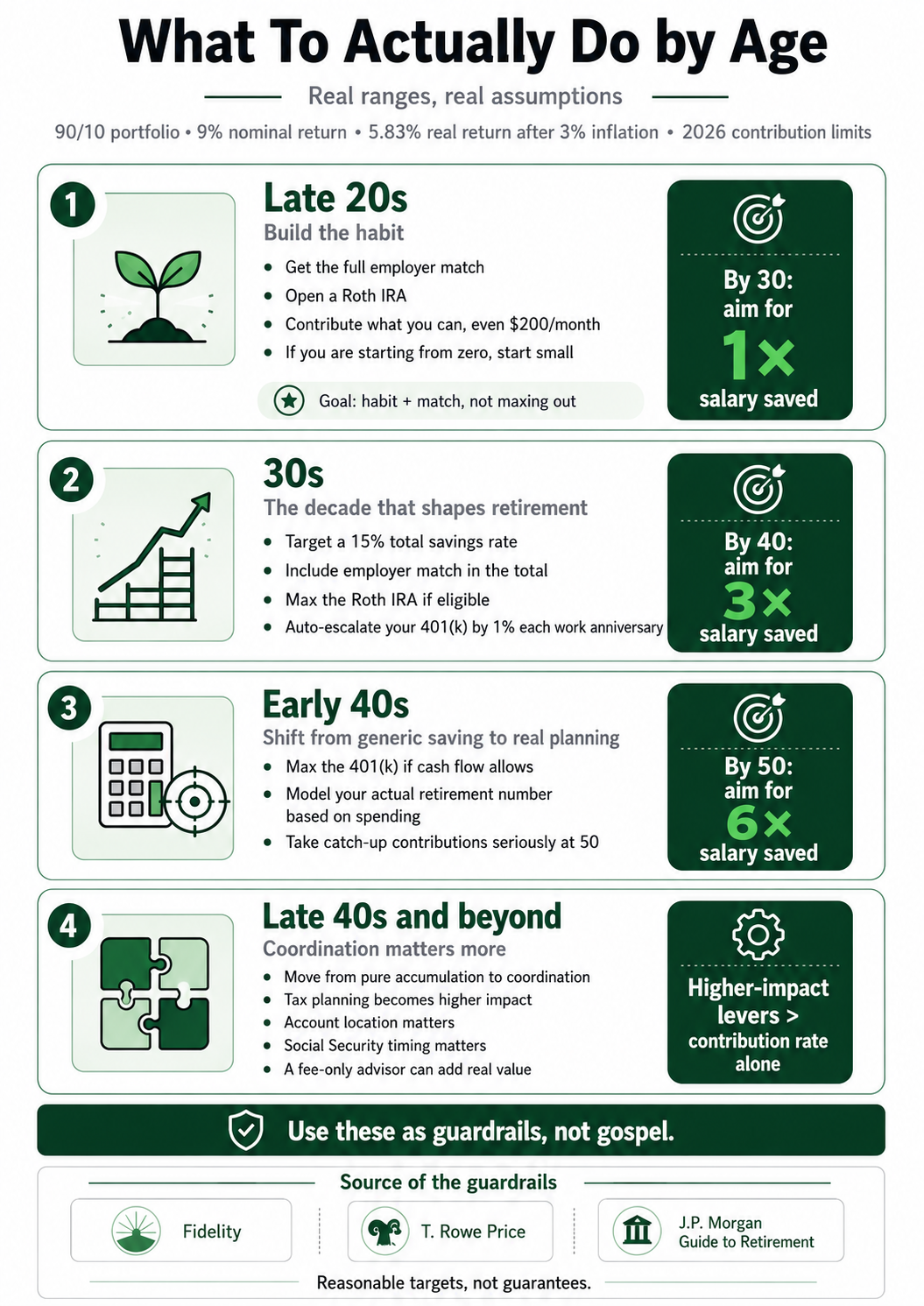

Most prospects come in already knowing roughly what they want to spend in retirement and roughly when. The math of the target portfolio is straightforward: about 25 times projected annual spending in today's dollars, adjusted for expected Social Security and any pension or annuity income.

What is not straightforward is the order of operations to get there efficiently. With a typical Melby Wealth client, we are coordinating:

A workplace 401(k) or 403(b) with both pre-tax and Roth options, plus a potential mega backdoor Roth via after-tax contributions.

A backdoor Roth IRA, because income usually exceeds the direct Roth phase-out.

A Health Savings Account, often underutilized as a stealth retirement account.

A taxable brokerage with embedded gains that need to be managed for tax-loss harvesting and asset location.

For business owners, a SEP IRA, Solo 401(k), or defined benefit plan with much higher contribution limits than the standard W-2 picture.

Generally speaking, the question is not "how much should I save" but "which dollar goes into which bucket in which order." Getting that sequencing right is worth measurable money over a 25- to 30-year planning horizon.

Tax Coordination Is Where the Real Value Lives

The headline retirement planning question for higher-earning households is rarely "should I save more?" It is almost always a tax question wearing different clothes.

Examples of the tax decisions that come up in our planning conversations:

Roth vs. traditional 401(k) split. For a household in the 32 percent bracket today with a clear path to a lower bracket in retirement, traditional dollars usually win on pure arbitrage. For a household expecting a similar or higher bracket in retirement (most higher-earning clients), Roth and mega backdoor Roth conversions usually win.

Asset location. Two portfolios with identical asset allocations can produce meaningfully different after-tax results based on which assets sit in which account. Bonds and REITs generally belong in tax-deferred space. Broad-market equity ETFs (VTI is a common default) generally belong in taxable accounts where qualified dividends and long-term capital gains get preferential treatment.

Roth conversions in the gap years. The window between retirement and the start of Required Minimum Distributions at age 73 (or 75, per SECURE 2.0 and birth year) is often the highest-impact tax planning opportunity in a client's lifetime. Converting traditional IRA dollars to Roth at controlled bracket-fills can save six figures over a 20-year retirement.

These are recurring annual decisions, and the answers shift with tax law, income, and portfolio makeup.

Equity Comp Changes the Picture

A meaningful slice of the households I work with have some form of equity compensation: RSUs, ISOs, NSOs, ESPP, or partnership interests. Equity comp interacts with retirement planning in ways that the basic "max your 401(k)" framework does not capture.

The questions I am asking with an equity comp client include:

Should we exercise ISOs in a strategically chosen year to take advantage of a lower AMT exposure window?

Are we selling RSUs immediately at vesting to diversify, or holding for long-term capital gains treatment, and what is the concentration risk in the meantime?

Is the ESPP discount a meaningful contribution to retirement savings or a distraction?

How do we model the equity comp as part of the overall household retirement projection, given that it is highly variable?

The right answer depends on the specifics, but the framework is the same: equity comp is a retirement planning input, not a separate problem.

Social Security Timing Is Real Money

For households with meaningful retirement assets, the Social Security claiming decision is mostly a timing decision, and the timing matters more than people think.

The 2025 Trustees Report projects combined trust fund depletion in 2034 with 81 percent of scheduled benefits payable thereafter, absent Congressional action. That is the conservative-case scenario most planners are using. For a married couple with mismatched earnings histories, delaying the higher-earner's benefit to age 70 is often the right call. The widow's benefit drives the math.

The point: a household with $2 million in retirement assets and a thoughtful Social Security claiming strategy can outpace a household with $2.3 million and a default-claim-at-FRA strategy. That is the kind of decision that justifies professional coordination.

When Professional Guidance Adds Value for Retirement Planning

Retirement planning is the topic where the cost of a fee-only advisor is most clearly justified by the math, in my experience. The high-impact areas:

Account sequencing across multiple plan types. When you have a 401(k), Roth IRA, HSA, taxable brokerage, and equity comp, the order of contributions and withdrawals is worth real dollars, not opinions.

Tax coordination between filing years. Roth conversion windows, charitable bunching, capital gain realization timing.

Behavioral coaching through market drawdowns. The dollars saved by not selling at the bottom in April 2020 or April 2025 are real, even if they do not show up on a single year's statement.

Estate and beneficiary coordination. Naming the right beneficiaries on the right accounts can save the next generation six figures in tax.

Periodic re-anchoring of the plan. Plans drift. Lives change. The retirement number you set at 35 is not the retirement number at 45. Someone needs to be in the seat to update it.

If you are at a point where the spreadsheet is no longer keeping up with the complexity, that is usually the signal it is time to bring in a fiduciary. For the consumer-facing version of this conversation, head over to Melby Money.

Worth saying clearly: roughly 71 percent of the people who schedule a first conversation with us have never worked with a financial advisor before. That is exactly who we work with. If you are wondering whether this is the right time or whether you are "ready," that is most people who reach out.

Schedule a retirement planning session →

About The Author

Shaun Melby, CFP® provides fee-only financial planning and investment management services in Nashville, TN through his company Melby Wealth Management. Shaun has over 15 years of experience as a financial advisor in Nashville. Shaun created Melby Money to educate the public about finances.

Full Disclosure: Nothing on this website should ever be considered to be advice, research, or an invitation to buy or sell any securities. Please see the Full Disclosure page for a full disclaimer.